Bail Industry Abuses

California Appeals Court Ruling Affirms Regulator’s Authority to Curb Bail Industry Abuses

California Appeals Court Ruling Affirms Regulator’s Authority to Curb Bail Industry Abuses

- In California, approximately 175,000 bail bond contracts are created each year, according to the California Department of Insurance. Nationally, the bail industry is estimated to underwrite around $14 billion in bail bonds annually, with an estimated revenue of $1.4–$2.4 billion.2 $1.4–$2.4 BILLION The bail industry exploits vulnerable Californians— usually people from low-income communities and communities of color that have been over-policed and over-incarcerated.

- The median bail bond amount in California is $50,000, with premiums commonly set around 10% of the total bail amount the court has determined. With bail amounts set so high, individuals seeking bail typically need cosigners— friends or family—to afford the bond premium. Cosigners frequently don’t understand or are misled about the true nature of their financial responsibility in paying the bond, as companies typically require the premium to be paid even if charges are resolved or dropped.

- Because many cannot afford a large one-time payment for the premium, much of the industry offers credit bail, where a company saddles families with monthly installment payments that can last for months or years. Yet, cosigners frequently have their consumer rights violated by bail bonds companies because law enforcement and regulatory agencies have failed to enforce consumer credit laws against the industry.

- The bail industry exploits vulnerable Californians—usually people from low-income communities and communities of color that have been over-policed and over-incarcerated—through predatory consumer financial transactions and abusive debt collection tactics, including lawsuits.

- While private bail bond companies are licensed under the Department of Insurance (CDI), no government entity has taken enforcement actions to address the consumer finance abuses perpetuated by these companies.

AB 539 - Fair Access to Credit Act 2020

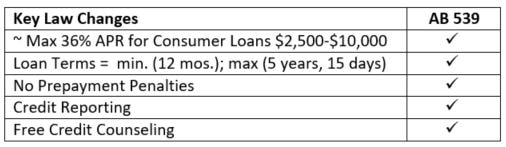

California law now limits interest rates on loans above $2,500!

With the passing of AB 539, loans $2,500-$10,000 now have an interest rate cap of 36% plus the Federal Funds Rate* (1.75% as of December 2019). High-cost lenders can no longer charge triple-digit annual interest rates ranging from 132% to 224%.

California has joined 37 other states that have a cap of 36% APR or less for loans in this range.[i]

The above chart outlines the legal changes that, starting January 1, 2020, will apply to non-bank finance lenders that are regulated and licensed in the state of California. Some examples of non-bank finance lenders include pawn shops, car title lenders, and check-cashing stores. This will suit both borrowers and lenders in order to expand safe and accessible consumer credit.

Post January 1, 2020, if you have seen, or personally received, a consumer loan for more than $2,500 that violates the legal guidelines established with AB 539, please reach out to:

- Californians for Economic Justice: Share Your Story

- CA Department of Business Oversight: https://docqnet.dbo.ca.gov/complaint/

- Consumer Financial Protection Bureau: https://www.consumerfinance.gov/complaint/getting-started/

AB 539 - Know Your Rights 1-pager (Eng/Spa) available in Resources tab.

*Federal Funds Rate refers to the interest rate banks charge other banks for lending them money from their reserve balances.

[i] National Consumer Law Center, “A Larger and Longer Debt Trap? Analysis of States’ APR Caps for a $10,000 Five-Year Installment Loan,” October 2018, https://www.nclc.org/issues/a-larger-and-longer-debt-trap-installment-loan.html

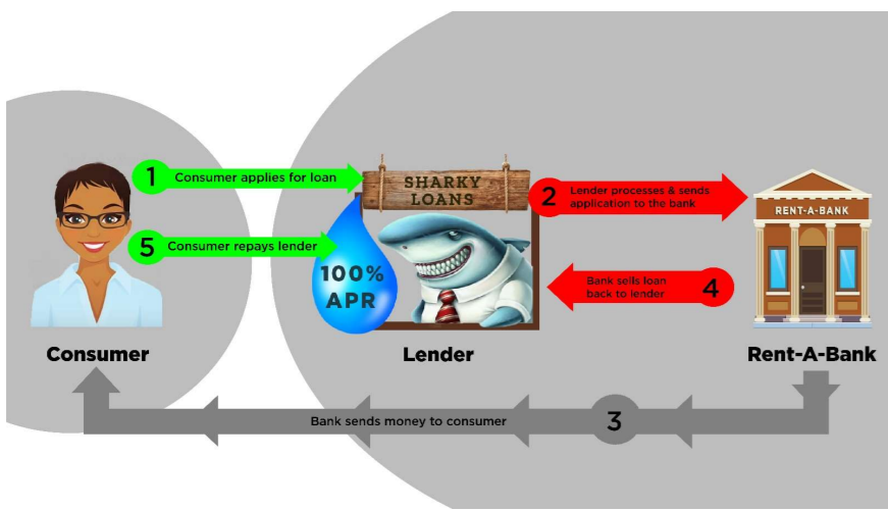

Rent-A-Bank Threat

What is it?

An arrangement that allows payday and other high-cost lenders to avoid state interest rate caps by partnering with federally-chartered banks (which, absent a federal interest rate cap, do not have to obey any limit aside from the Military Lending Act). Essentially, these lenders are using the bank partnership to continue making predatory loans with triple digit APRs in states where those high rates are illegal.

How does it work?

Through a rent-a-bank scheme, high cost lenders can market and take in applications for loans, while the bank they are partnered with approves the costly loan and grants money to the borrower. Before the borrower begins to repay, the bank sells the loan back to the lender so that the borrower repays the lender.

History

These partnerships began emerging in the late 1990s. Federal bank regulators cracked down on these models in the early 2000s, but they are now on the rise again across the country.

Current Threat to AB 539 Law

Before AB 539 was even signed into law in the fall of 2019, three online lenders announced plans to their shareholders to evade the soon-to-be-passed state rate cap in California. Elevate, Curo and Enova companies shared their plans to establish rent-a-bank partnerships to continue making profits with high cost loans. Advocacy groups like CA4EJ, along with state legislators, have sounded the alarm to the Department of Business Oversight and the Attorney General’s office to crack down on these, and potentially other, lenders’ plans.

Post January 1, 2020, if you have seen, or personally received, a consumer loan for more than $2,500 that violates the legal guidelines established with AB 539 (of ~36% APR), this may be a sign of a rent-a-bank scheme at work.

Please notify:

An arrangement that allows payday and other high-cost lenders to avoid state interest rate caps by partnering with federally-chartered banks (which, absent a federal interest rate cap, do not have to obey any limit aside from the Military Lending Act). Essentially, these lenders are using the bank partnership to continue making predatory loans with triple digit APRs in states where those high rates are illegal.

How does it work?

Through a rent-a-bank scheme, high cost lenders can market and take in applications for loans, while the bank they are partnered with approves the costly loan and grants money to the borrower. Before the borrower begins to repay, the bank sells the loan back to the lender so that the borrower repays the lender.

History

These partnerships began emerging in the late 1990s. Federal bank regulators cracked down on these models in the early 2000s, but they are now on the rise again across the country.

Current Threat to AB 539 Law

Before AB 539 was even signed into law in the fall of 2019, three online lenders announced plans to their shareholders to evade the soon-to-be-passed state rate cap in California. Elevate, Curo and Enova companies shared their plans to establish rent-a-bank partnerships to continue making profits with high cost loans. Advocacy groups like CA4EJ, along with state legislators, have sounded the alarm to the Department of Business Oversight and the Attorney General’s office to crack down on these, and potentially other, lenders’ plans.

Post January 1, 2020, if you have seen, or personally received, a consumer loan for more than $2,500 that violates the legal guidelines established with AB 539 (of ~36% APR), this may be a sign of a rent-a-bank scheme at work.

Please notify:

- Californians for Economic Justice: Share Your Story

- CA Department of Business Oversight: https://docqnet.dbo.ca.gov/complaint/

- Consumer Financial Protection Bureau: https://www.consumerfinance.gov/complaint/getting-started/

SB 472 - Earned Income Access Service Providers Act 2021

The Californians for Economic Justice coalition is monitoring state legislation that aims to create a regulatory framework for fin-tech companies like Earnin that offer early access to California employees’ earned wages.

With mobile and online app products marketed as healthy alternatives to high cost loans, these companies offer borrowers advanced wages, utilizing either a “direct-to consumer” or a “direct-through-employer” model.

How does it work?

In the employer-based model, a borrower’s employer partners with a third party to input wage information, on the employee’s behalf, so that earned wages are available before their scheduled payday. In the direct-to consumer model, borrowers self-report their wages in the app, and must connect the product to an existing bank account. The catch is that there is often a fee or “tip” associated with each withdrawal, which can make these loans expensive and also gives the wage advance company direct access to a borrower’s bank account.

Payday Loan via App

Consumer advocates are calling on legislators to classify these products as the loans that they are, simply available via a new platform. Classifying these products as loans will make them subject to compliance with California lending laws, including but not limited to: requiring an interest rate cap (since a withdrawal fee is essentially added interest to one’s earned wages), bank account protection, and language accessibility, in addition to other consumer protections.

With mobile and online app products marketed as healthy alternatives to high cost loans, these companies offer borrowers advanced wages, utilizing either a “direct-to consumer” or a “direct-through-employer” model.

How does it work?

In the employer-based model, a borrower’s employer partners with a third party to input wage information, on the employee’s behalf, so that earned wages are available before their scheduled payday. In the direct-to consumer model, borrowers self-report their wages in the app, and must connect the product to an existing bank account. The catch is that there is often a fee or “tip” associated with each withdrawal, which can make these loans expensive and also gives the wage advance company direct access to a borrower’s bank account.

Payday Loan via App

Consumer advocates are calling on legislators to classify these products as the loans that they are, simply available via a new platform. Classifying these products as loans will make them subject to compliance with California lending laws, including but not limited to: requiring an interest rate cap (since a withdrawal fee is essentially added interest to one’s earned wages), bank account protection, and language accessibility, in addition to other consumer protections.

Quality Student Loan Servicing

Student loan servicers routinely lose paperwork, misapply payments, give inaccurate information, and even steer borrowers into repayment options that add to the overall cost of their loans. Unlike mortgages or credit cards, there is no industry-wide framework at the federal level to regulate the student loan industry. As a result, people with student loans do not have safeguards to help them get out of debt.

Californians for Economic Justice strongly supports efforts to establish a set of rights for Californians holding student debt, by requiring student loan companies to treat borrowers fairly and giving borrowers the right to hold these companies accountable when they fail to meet basic servicing standards.

Learn more about the campaign to pass a California Borrower Bill of Rights here: www.californiaborrowers.org

Californians for Economic Justice strongly supports efforts to establish a set of rights for Californians holding student debt, by requiring student loan companies to treat borrowers fairly and giving borrowers the right to hold these companies accountable when they fail to meet basic servicing standards.

Learn more about the campaign to pass a California Borrower Bill of Rights here: www.californiaborrowers.org

Financial Security for All

Debt Collection

Currently debt collectors are able to take funds directly from a consumers' bank account through a bank levy. This “Debt Collector Takes All” scheme leaves low-income people without any money - money they were counting on to pay their rent and other basic living expenses.

Californians for Economic Justice strongly supports protections that would provide a minimal amount of money that must be left in a bank account if it is levied by a debt collector.

Criminal Justice Fines and Fees

Years of research on criminal justice fines and fees in California, and the experiences of individuals in the criminal justice system, have found that these fees are unjust, high pain, and low gain. Eliminating administrative fees will allow people who are formerly incarcerated to devote their already limited resources to critical needs like food, education, housing, and health insurance for themselves and their families. Repealing criminal fees will result in improved employment prospects for formerly incarcerated people and put more money in the pockets of economically insecure families, aiding successful reentry and reducing California’s recidivism rate.

Californians for Economic Justice strongly supports an end to the assessment and collection of administrative fees imposed against people in the criminal justice system, and to expunge all previously assessed related debt.

Currently debt collectors are able to take funds directly from a consumers' bank account through a bank levy. This “Debt Collector Takes All” scheme leaves low-income people without any money - money they were counting on to pay their rent and other basic living expenses.

Californians for Economic Justice strongly supports protections that would provide a minimal amount of money that must be left in a bank account if it is levied by a debt collector.

Criminal Justice Fines and Fees

Years of research on criminal justice fines and fees in California, and the experiences of individuals in the criminal justice system, have found that these fees are unjust, high pain, and low gain. Eliminating administrative fees will allow people who are formerly incarcerated to devote their already limited resources to critical needs like food, education, housing, and health insurance for themselves and their families. Repealing criminal fees will result in improved employment prospects for formerly incarcerated people and put more money in the pockets of economically insecure families, aiding successful reentry and reducing California’s recidivism rate.

Californians for Economic Justice strongly supports an end to the assessment and collection of administrative fees imposed against people in the criminal justice system, and to expunge all previously assessed related debt.

Copyright © 2020 Californians for Economic Justice. All Rights Reserved.